House Bill 488 sponsored by Ohio State Representatives Becker and Hood will require that the effect of proposed tax levies be more clearly explained on the ballot.

Under current law, information on the effect of a proposed tax levy is expressed based upon the “tax value” of real property (35% of the true value). The proposed law will provide information based on the effect of the tax levy using the fair market of real property, as well as the millage rate against the tax value.

The proposed change will make it easier for voters to understand tax levies and make more informed choices at the ballot box.

You can follow the progress of House Bill 488 here.

“Joint and several liability” is a legal concept that provides that each obligor under a contract is fully liable for the obligations under that contract as to the other party to the contract (i.e, the party to whom the joint obligors are obligated). So, in the instance that two or more guarantors sign a guarantee instrument to a bank for a loan, if they are “joint and severally liable,” it means that each guarantor owes the entire debt to the bank in the event of default. The bank can’t collect twice the guaranteed amount, but it can choose which guarantor from which to obtain payment.

So, the question addressed in this article is “what is the default position as to joint and several liability on a contract if the instrument is silent on the topic?” We address topic this under Ohio and Kentucky law.

The answer: In short, “joint and several” is the default interpretation absent language in the instrument that absolves parties of such liability.

General Contract Principles

A contract is a promise or a set of promises for the breach of which the law gives a remedy, or the performance of which the law in some way recognizes as a duty. Restat 2d of Contracts, § 1 (2nd 1981). Further, where there are more promisors than one in a contract, some or all of them may promise the same performance, whether or not there are also promises of separate performances. Restat 2d of Contracts, § 10 (2nd 1981). Such is the situation when more than one individual signs a guaranty or a promissory note.

Standard contract language

The standard modern form to create duties which are both joint and several is “we jointly and severally promise,” but any equivalent words will do as well. In particular, a promise in the first person singular, signed by several persons, creates joint and several duties. Restatement (Second) of Contracts § 289 (1981). What this means is that, generally, under the common law, promises of the same performance create “joint” liability on the part of each promisor unless an intention is manifested to create a “solidary” obligation. Restat 2d of Contracts, § 289 (2nd 1981). However, many states have state specific statutes which have altered or refined this rule.

Common law when contract is silent

In Ohio, an individual signing a note as a co-maker with another individual is jointly and severally liable for the debt, except as otherwise provided in the instrument. Ohio Rev. Code Ann. § 1303.14(A). Star Bank, N.A. v. Jackson, 2000 Ohio App. LEXIS 5567, *1. Under U.C.C. Art. 3, a party signing a promissory note as a co-maker is jointly and severallyliable for the debt. Darrah v. Leakas, 1994 Ohio App. LEXIS 220, *1. As among themselves, co-makers are presumed liable in equal amounts, however, these rights are governed by the particular terms of the contract between the co-makers. Poppa vs. Hilgeford, 1982 Ohio App. LEXIS 13658, *1.

In Kentucky, likewise, in the absence of an express agreement to the contrary, when two or more individuals execute a note, such persons are jointly and severally liable to the holder, even though the instrument contains no such express provision. KRS 355.3-118. Schmuckie v. Alvey, 758 S.W.2d 31, 33-34.

Duty of contribution from co-makers

As between or among themselves, however, in the absence of evidence of a contrary agreement, co-makers are presumed to be liable in equal amounts and a right of contribution, based upon an implied contract of reimbursement and not the instrument, exists between or among them. 11 Am. Jur. 2d, “Bills & Notes” § 588 (1963). Id.

Conclusion

What this means is that if you sign a note or guaranty or other like instrument with another individual, the holder of that note, in their sole discretion, can choose to recover the full amount against you and only you. As between you and your co-maker, depending on your agreement, you likely retain the right to seek contribution from them pro-rata.

For more information on commercial instruments and personal guarantees, contact Julie Gugino at (513) 943-5669.

Through the course of our representation of clients, they often encounter zoning codes which are outdated and properties that are non-conforming, often in vibrant flourishing neighborhoods. This was the case for one client, who desired to seek a use variance for a property in Evanston, a stone’s throw from the burgeoning Walnut Hills neighborhood.

The challenge

In this case, the clients desired to purchase a block construction building that was zoned Residential Mixed Use and convert the same into an artisanal cheese making facility and retail store/tasting room. This building had previously been operated as a medical building and was constructed prior to implementation of the current Zoning Code. As a result, an 8,334 square foot block building sat vacant and unused, a blight to its community because of zoning that relegated it to Residential Mixed Use. As a result, we were retained to pursue a use variance on their behalf and assist them in their endeavors to “put Cincinnati cheese on the map and to begin that dream in the Evanston neighborhood.”

Variances under Cincinnati Municipal Code

Under §1445-15 of the Cincinnati Zoning Code a variance from the requirements of the Cincinnati Zoning Code can be granted, provided the condition giving rise to the request for the variance was not created by the current or prior owner. In addition, a variance can be granted owing to special conditions affecting the property, where application of the Zoning Code would be unreasonable and result in practical difficulties. Finally, consideration is given as to whether the variance is necessary for the preservation and enjoyment of a substantial property right of the applicant possessed by owners of neighboring properties.

Showing of unnecessary hardship

In addition to these factors, under §1445-16 of the Code, no variance can be granted unless the applicant demonstrates it will suffer unnecessary hardship if strict compliance with the terms of the Code is required. Hardship is demonstrated by the following factors: (a) the property cannot be put to any economically viable use under any of the permitted uses in the zoning district; (b) the variance requested stems from a condition that is unique to the property at issue and not ordinarily found in the same zone or district; (c) the hardship condition is not created by actions of the applicant; (d) the granting of the variance will not adversely affect the rights of adjacent property owners or residents; (e) the granting of the variance will not adversely affect the community character, public health, safety or general welfare; (f) the variance will be consistent with the general spirit and intent of the Zoning Code; and (g) the variance sought is the minimum that will afford relief to the applicant.

“In The Public Interest”

Finally, in order to obtain a use variance, an applicant must show the proposed variance “is in the public interest.” The factors considered under §1445-13 of the Code include: present zoning, community guidelines and plans, existing traffic, buffering, landscaping, hours of operation, neighborhood compatibility, proposed zoning amendments, consideration of adverse effects, the elimination of blight, economic benefit, job creation, effect upon tax valuations, and private and public benefits.

The wasted potential of a long-vacant property

In our clients zoning matter, an existing structure which did not conform to the Code had sat vacant for five years or more. The zoning needs of the Property were unique to it and the hardship had not been created by the owner of the Property. Its impact on the immediate neighborhood as a vacant and blighted building were adverse, contributing nothing to the neighborhood, and detracting greatly from the same.

Making a difference for our client

Our clients were able to obtain a use variance and now that vacant building has been transformed into a cheese making facility and retail store/tasting room that will further transform this already bustling community.

Ohio imposes fees on the conveyance of real estate, and generally determines the value of real property based upon the sale price when the property is sold. One means of avoiding the conveyance fee and reporting the sale price is the use of a “LLC Loophole.”

The LLC Loophole is a means of conveying title to real property using an LLC as an intermediary, rather than transferring title directly from the seller to the buyer. A property owner transfers title to real estate to an LLC that she owns, and then sells the LLC itself to the buyer. One benefit of this conveyance is that no conveyance fee is paid, and the auditor is not alerted to the sale price.

Consider this illustration:

Property owner owns a strip mall valued by the auditor at $500,000. She has received an offer to buy the property for $750,000, but the buyer wants to avoid the publicity of reporting the sale through a conveyance form and the automatic increase in tax value that would come by simply buying the property directly from the property owner. So, the property owner sets up a new limited liability company, Strip Mall, LLC; conveys title to the property to Strip Mall, LLC; and then sells her 100% ownership interest in Strip Mall, LLC to the buyer for $750,000. The only filing with the county auditor is the conveyance fee showing a fee exempt transfer from the property owner to the LLC. No one is alerted that the buyer now owns the strip mall or that it was valued at $750,000 in an arm’s length transaction.

Under the proposed law, when the property owner sells her ownership interest in the LLC, she would have to report that sale to the auditor as if she had sold the real estate directly to the buyer. At that point, the auditor would assess a conveyance fee, and the real estate would be taxed at the sale price. The proposed bill would require the reporting and payment of taxes whenever any interest in an LLC or other entity that owns real estate (directly or indirectly) takes place.

To be clear, there is nothing unlawful about using LLCs in property transfers, and it is a perfectly legitimate method for conveying real estate.

We expect that public school boards in particular, as well as other property tax funded organizations will lobby in support of this legislation; and that it will find opposition from real estate investors and small government advocates generally. Whether it is this particular bill or another future proposal, the LLC Loophole will be facing continued scrutiny and efforts to impose conveyance fees and determine the purchase price.

The Legislative Services Commission’s analysis and the bill text are below.

Finney Law Firm will be keeping an eye on this bill as it works through the Ohio Legislature.

As we march through our lives, folks shove documents under our nose for signature all the time. In reality, we should carefully, very carefully, read them and consider their implications before signing any of them.

After all, there are charlatans and fraudsters standing eager to take advantage of us at every turn. And even if other parties don’t start out as such, life events can put people in default or desperate straits – and then “desperate people do desperate things” as they say.

Still, certain documents bear significant additional risk or have a history of resulting in litigation or economic calamity for the signer.

Here, we take a serious look at six transactional documents that frequently result in legal or financial problems:

Personal guarantee for debts of another. Your daughter and son-in-law are buying a house, but have bad credit, or you are starting a business and need to guarantee the lease or franchise agreement to provide the fiscal backing for the undertaking. A personal guarantee is fine and in some instances both called for and reasonable. But think it through:

–> Am I financially capable of fulfilling this guarantee if the underlying obligation falls into default?

–> Would the other party accept a guarantee limited in time, amount or some other cutoff? Or proceed with no guarantee?

–> If there are multiple guarantors, would the lender be satisfied with me just paying my pro-rata share of the underlying debt?

–> Is there some other way that the transaction can proceed without my guarantee? Can someone offer security for the loan instead?

Non-Compete agreements. More and more employers are asking new employees to sign non-compete agreements or agreements wherein the employee agrees not to solicit customers, employees or vendors of the enterprise. Employers are entirely within their rights to demand such agreements (the question of whether they are enforceable is addressed here). But should an employee agree to restrict his future earnings potential and career path based upon this job opportunity? If you really think it through, many time the answer is “No thanks, I’ll take a pass.”

Agreements with attorneys. We really hate to say this, but one of our clients was a seller under a land installment contract for the sale and purchase of real estate. The buyer was an attorney. After repeatedly falling into default, our client initiated a forfeiture action against the attorney. He countered with a blistering series of arguments that were all untrue or frivolous. Confronted with withering legal bills to prove their case, they quickly settled on relatively unfavorable terms. Lesson learned.

Businesses with 50/50 ownership. It seems to make sense: Two partners throwing in equal shares of cash and effort to start a business; they should own it 50/50. And in decision-making, decisions are 50/50, meaning it requires the consent of both parties to move forward with anything. However, after years of addressing business disputes, it has become clear that these ownership structures – with no one in charge and everyone’s cooperation required to make decisions – are the source of operational and legal gridlock, resulting in painful, expensive and endless litigation. I have even seen very difficult dispute resolution between former (or soon-to-be-former) spouses in a 50/50 ownership structure. Indeed, getting into business with any third party can be the source of conflict, monetary losses and litigation.

Agreements you are not prepared to litigation to conclusion. If you think about it, in an instance in which you are investing time or money, you have two essential choices: Either be prepared to “eat” these investments by walking away or be prepared to litigate your claims to conclusion to defend your investment. Is the person you are contracting with someone you are prepared to sue to enforce your rights? Is the transaction structured and documented in such a way that you could prevail in that litigation? Will the cost of enforcing these agreements (or defending against a suit from the other party) of such magnitude that it will be worth litigating?

Indemnity and “hold harmless” clauses in leases and other contracts. It’s easy to sign a 50-page legal document that satisfies the major business terms you have negotiated. But what about the fine print? Buried deeply within a lease, loan documents, or asset purchase contracts can be all sorts of warranties, indemnities, and “hold harmless” provisions. It seems simple that a seller or borrower should stand behind his obligations, but do you really want to give an open-ended contractual indemnity or warranty in this specific instance? It is, as is addressed here, a potential blank check, open-ended access to your checkbook.

We are not saying that you should never sign any of the foregoing instruments. What we are saying is that experientially these undertakings result in much conflict, legal fees and emotional angst, and should be undertaken only with great caution.

On multiple occasions, Finney Law Firm has been approached by a beneficiary of a trust when the beneficiary is concerned with the administration of the trust by the trustee. In these types of situations, our firm has helped the beneficiary pursue and protect the beneficiary’s rights.

Although there are other rights, below you will find a summary of some of the statutory rights of a trust beneficiary.

Under current Ohio law, a trustee shall, within sixty (60) days after accepting its duties as trustee, notify the current beneficiaries of a trust of the trustee’s acceptance of the trust, together with the trustee’s name, address, and telephone number.

Further, within sixty (60) days after the date the trustee acquires knowledge of the creation of an irrevocable trust, or the date the trustee acquires knowledge that a formerly revocable trust has become irrevocable, the trustee must notify the current beneficiaries of the existence of the trust, the identity of the settlor/grantor, the right to request a copy of the trust instrument, and the right to receive a trustee’s report as defined below.

Upon the request of a beneficiary, the trustee shall provide to the beneficiary a copy of the trust document. Unless the beneficiary specifically requests a copy of the entire trust document, the trustee may furnish to the beneficiary a copy of a redacted trust document that includes only those provision of the trust that are relevant to the beneficiary’s interest in the trust. If the beneficiary requests a copy of the entire trust document after receiving a copy of the redacted portion, the trustee must furnish a copy of the entire trust document.

The trustee is also required to send a trust report at least annually and at the termination of the trust, to the current beneficiaries, and also to other beneficiaries who request it. This is commonly known as an accounting. The report shall detail the trust property, liabilities, receipts, and disbursements, including the source and amount of the trustee’s compensation, a listing of the trust assets and, if feasible, their respective market values.

Any beneficiary may waive the right to a trustee’s report or other information otherwise required to be furnished to a beneficiary. A beneficiary, with respect to future reports and other information, may withdraw a waiver previously given.

A trustee, in fulfilling its fiduciary obligations, must keep the current beneficiaries reasonably informed about the administration of the trust and of the material facts necessary for them to protect their interests.

Please note that the above rights are not a comprehensive list of the rights of a beneficiary of a trust.

_________

For assistance with an Ohio trust or more generally Ohio estate planning and estate administration needs, contact Isaac T. Heintz (513-943-6654; [email protected]) or Eli Krafte-Jacobs (513-797-285; [email protected]) of our transactional team.

Finney Law Firm attorney Stephen E. Imm will present to Cincinnati’s Empower U on April 10, 2018 on the topic: “What Employers Can Learn From Hollywood’s Sexual Harassment Problem.”

The seminar will be presented at the EmpowerU studios at 225 Northland Blvd., Cincinnati, OH 45246 at 7 PM.

Empower U was founded by our firm client and friend Daniel Reginald of Frame USA to provide a full annual program of free education programs to empower citizens to understand and impact their communities.

They have invited experienced employment law attorney Stephen Imm to speak on April 10 on the hottest topic in America today: Sexual harassment in the workplace. Steve Imm has more than 30 years of experience working on employment law issues and so the #MeToo movement is old hat to him.

We will send sign-up information as it becomes available. Please plan on joining us for this free seminar.

Tax bills just hit the mailboxes of Hamilton County taxpayers this week, and our phone is ringing with questions about our Ohio property tax valuation reduction services.

Sample calls:

Many of the cases have merit, and we are aiding those taxpayers in getting their taxes reduced. Others, not so much. Here’s a sample call:

Client: “Hey, I just got my tax bill and my valuation just went up by 40%. Can I challenge it?”

Attorney: “It depends. How does the Auditor’s new valuation of your property compare to the property’s true value?”

Client: “What do you mean ‘true value?'”

Attorney: “I mean, if you put the property on the market and offered it for sale, is the Auditor’s valuation lower than or higher than that value?.”

Client: “Oh, I would never sell it for that number. I mean, my property is worth a whole lot more than that.”

Attorney: “Then, don’t bring the case. The Board of Revision compares the Auditor’s valuation to the true value and adjusts the valuation accordingly. For single family homes, they use comparable sales of other properties. Actual sales.”

Client: “But my valuation went up by 40%! I mean there is no way my property increased in value 40% in three years.”

Attorney: “Well, that may be true, but how do we know the Auditor had not undervalued your property three years ago, and is just getting it right now?”

Client: “But the Auditor has my neighbor’s property valued for less than mine and the houses are the same.”

Attorney: “None of those things matter. They really don’t. The Board of Revision can’t even consider those things. The only question is the comparison of your home’s true worth versus how the Auditor has assessed it and that comparison hinges off of comparable sales in your neighborhood.”

Some basic concepts:

The concepts are hard to swallow sometimes:

The Board of Revision takes a fresh look at valuation when a challenge is brought.

How the Auditor’s current value compares to the true value of the property (typically as established by comparable sales in your neighborhood) is the only yardstick of value in the current cycle.

The percentage increase of your property valuation from the prior cycle is completely irrelevant to that analysis. Completely.

The Auditor’s opinion of the value of your neighbor’s property also is completely irrelevant to that question

Both data and arguments relating to those issues are inadmissible before the Board of Revision. If you try to talk about those things at your hearing, you will be shot down by the panel. Period. Just don’t go there.

The Auditor does not have to justify how he came up with his valuation of your property. In fact, he is completely within his rights and authority under Ohio law to choose any value he wants for your property for absolutely no justification at all. That’s simply how the law is written. It is the statutory prerogative of the Auditor. If you don’t like it, then YOU can run for Auditor.

At a hearing, it is the taxpayer’s burden to prove the correct valuation. The Auditor does not have to prove anything.

NOTE: The result of a Board of Revision challenge to your property’s valuation could well be an increase, rather than a reduction. Be forewarned.

From 2008 to 2015 — throughout the real estate recession (some would say depression) — it was relatively easy to get valuations reduced for many properties. However, with the rising tide of real estate prices, those hoping for quick and easy savings should think twice. They may well get a surprise — an increase rather than a reduction.

If you don’t like the law, don’t be mad at us. We are not legislators or judges. We didn’t make these rules.

Free how-to video:

Here is a complete videotaped seminar presented by attorney Christopher P. Finney on property tax valuation reduction with step-by-step instructions.

More help:

For questions (other than those in the sample call, above!), feel free to contact Christopher P. Finney (513-943-6655).

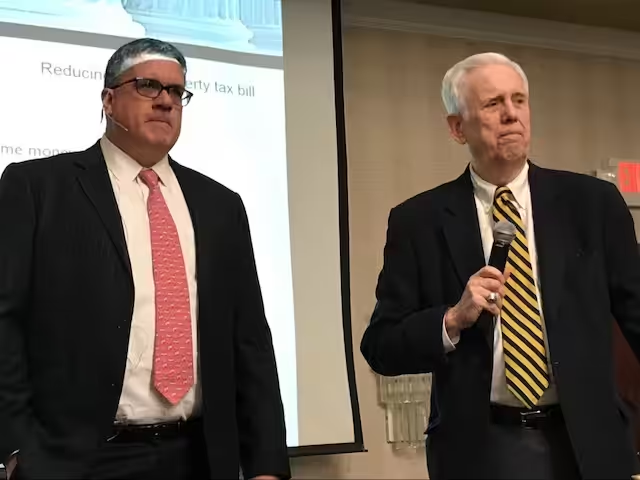

Tonight, Hamilton County Auditor Dusty Rhodes and attorney Chris Finney presented to the Greater Cincinnati Real Estate Investors Association on the topic of “Property Tax Reduction.”

The presentation went in-depth in instructing property owners on the procedure to reduce the Auditor’s valuation of real property in Ohio to achieve tax savings.

We thank the County Auditor for appearing with us in this important public service! And we thank REIA founder Vena Jones-Cox and REIA President Scott Ellsworth for making this presentation possible.

Property owners are reminded that March 31 of each year is the deadline in Ohio for tax challenges. You may call Chris Finney (943-6655) for more information.

Tonight, Hamilton County Auditor Emerson “Dusty” Rhodes and Finney Law Firm attorney Chris Finney present on “Property Tax Reduction” at the Greater Cincinnati Real Estate Investors Association (REIA) at 6 PM at the Ramada Plaza at 11320 Chester Rd., Cincinnati, OH 45246 on Thursday, January 4 at 6 PM.

A dinner is served beforehand at 5:30 PM.

The meeting is open for free to REIA members and first-time attendees can obtain a free guest pass here. REIA’s program announcement is here. REIA’s web site is here.